The idea of Bitcoin on US bank balance sheets has steadily moved from a fringe concept to a serious topic of discussion among financial institutions. As digital assets continue to reshape global finance, major players like Morgan Stanley are openly analyzing the feasibility, risks, and long-term implications of integrating Bitcoin into traditional banking frameworks. While the firm acknowledges the inevitability of this shift, it also emphasizes that the transition is not imminent.

This nuanced stance reflects the broader reality of the financial ecosystem, where innovation often collides with regulation, risk management, and institutional inertia. In this article, we explore why Bitcoin adoption by US banks appears inevitable, what barriers remain, and how the timeline may unfold.

The Growing Institutional Interest in Bitcoin

Institutional interest in Bitcoin has surged over the past decade, driven by its reputation as a store of value, inflation hedge, and digital gold alternative. Large asset managers, hedge funds, and even pension funds have gradually incorporated Bitcoin into their portfolios.

A Shift From Skepticism to Strategic Allocation

Not long ago, Bitcoin was dismissed by traditional finance as speculative or even irrelevant. However, firms like Morgan Stanley have shifted their stance, recognizing Bitcoin as a legitimate asset class. This evolution reflects broader acceptance across Wall Street, where digital asset exposure is increasingly viewed as a competitive advantage.

The growing demand from institutional clients is one of the primary drivers behind this shift. High-net-worth individuals and corporate investors are actively seeking crypto investment opportunities, pushing banks to expand their offerings.

The Role of Custodial Services

Before Bitcoin can appear on bank balance sheets, institutions must develop robust crypto custody solutions. Custody refers to the secure storage of digital assets, a critical component given the risks associated with private keys and cyber threats.

Major banks have already begun offering custody services, signaling an important step toward broader integration. However, custody alone does not equate to holding Bitcoin as a balance sheet asset—it merely facilitates client exposure.

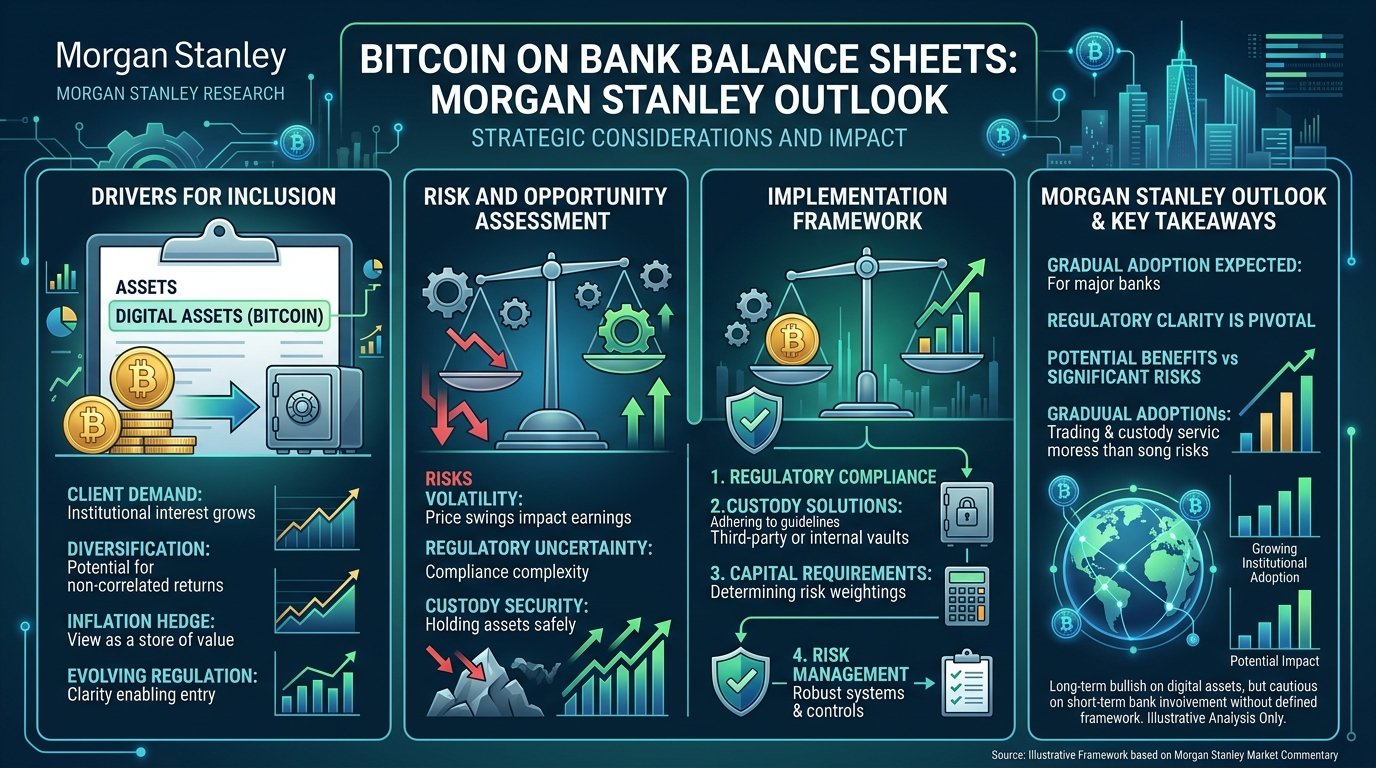

Why Bitcoin on US Bank Balance Sheets Is “Coming”

Morgan Stanley’s analysis suggests that the integration of Bitcoin into bank balance sheets is not a question of if, but when. Several structural trends support this outlook.

Increasing Regulatory Clarity

Regulation has long been the biggest obstacle to Bitcoin adoption in banking. However, progress is being made. US regulators are gradually providing clearer frameworks for how banks can interact with digital assets.

As regulatory uncertainty diminishes, banks gain the confidence needed to explore direct Bitcoin holdings. Clear rules around capital requirements, risk-weighting, and compliance will be essential in enabling this transition.

Competitive Pressure Among Banks

The financial industry is highly competitive, and banks are constantly seeking new revenue streams. As more institutions embrace blockchain technology and digital assets, others risk falling behind.

If even a handful of major banks begin holding Bitcoin on their balance sheets, it could trigger a domino effect. This competitive dynamic is a key reason why Morgan Stanley believes adoption is inevitable.

The Evolution of Bitcoin as a Mature Asset

Bitcoin has matured significantly since its early days. With increased liquidity, improved infrastructure, and broader market participation, it is now viewed as a more stable and reliable asset.

The development of regulated financial products, such as Bitcoin ETFs, has further legitimized the asset. These advancements make it easier for banks to justify Bitcoin integration into financial systems.

Why It’s Not Happening Yet

Despite the strong case for future adoption, Morgan Stanley emphasizes that several barriers still prevent banks from adding Bitcoin to their balance sheets today.

Regulatory Constraints Still Loom Large

While progress has been made, the regulatory environment remains complex. Banks must comply with strict capital requirements, and Bitcoin’s volatility presents challenges in this regard.

Regulators are also cautious about systemic risk. Allowing banks to hold Bitcoin directly could expose the financial system to new forms of instability, particularly during periods of market turbulence.

Volatility and Risk Management Concerns

Bitcoin’s price volatility remains a major concern for banks. Unlike traditional assets, Bitcoin can experience significant price swings within short periods.

For banks, which prioritize stability and risk mitigation, this volatility complicates the case for balance sheet inclusion. Risk models must be adapted to account for Bitcoin’s unique characteristics.

Accounting and Reporting Challenges

Accounting standards for digital assets are still evolving. Questions around how to value Bitcoin, recognize gains or losses, and report holdings create additional complexity.

Without standardized accounting frameworks, banks face uncertainty in how Bitcoin would impact their financial statements. This lack of clarity is a significant deterrent.

The Role of US Regulation in Shaping the Timeline

The pace at which Bitcoin appears on US bank balance sheets will largely depend on regulatory developments. Agencies such as the U.S. Securities and Exchange Commission and the Federal Reserve play a crucial role in setting the rules.

Balancing Innovation and Stability

Regulators must strike a delicate balance between encouraging innovation and protecting the financial system. While they recognize the potential benefits of digital assets, they are also wary of the risks.

This cautious approach explains why progress has been gradual. Policymakers are taking the time to fully understand the implications of Bitcoin in banking systems before granting widespread approval.

The Impact of Global Competition

Interestingly, developments in other countries could influence US policy. If foreign banks begin integrating Bitcoin into their balance sheets, US regulators may feel pressure to keep pace.

Global competition could accelerate the timeline, particularly if digital asset adoption becomes a key differentiator in international finance.

How Banks Are Preparing Behind the Scenes

Even though Bitcoin is not yet on their balance sheets, US banks are actively preparing for that future.

Investment in Blockchain Infrastructure

Banks are investing heavily in blockchain technology, which underpins Bitcoin and other digital assets. This includes building internal expertise, developing new platforms, and forming strategic partnerships.

These investments position banks to move quickly once regulatory conditions allow for direct Bitcoin holdings.

Expanding Crypto-Related Services

Many banks already offer crypto-related services, such as trading, custody, and advisory. These services provide valuable experience and insights that will be essential when transitioning to balance sheet exposure.

By gradually expanding their involvement, banks can manage risk while staying ahead of market trends.

The Potential Impact on the Financial System

The inclusion of Bitcoin on bank balance sheets would have far-reaching implications for the financial system.

Increased Legitimacy for Bitcoin

If major banks begin holding Bitcoin, it would significantly enhance its credibility. This could lead to increased adoption among both institutional and retail investors.

Changes in Risk Dynamics

Bitcoin’s unique properties could alter how banks manage risk. While it introduces new challenges, it also offers diversification benefits.

Integration With Traditional Finance

The integration of Bitcoin into banking systems would mark a major step toward the convergence of traditional finance and digital assets. This could unlock new opportunities for innovation and growth.

What This Means for Investors

For investors, Morgan Stanley’s outlook provides valuable insights into the future of Bitcoin adoption.

A Long-Term Perspective Is Essential

The message is clear: while Bitcoin on bank balance sheets is coming, it will take time. Investors should adopt a long-term perspective and avoid expecting immediate changes.

Monitoring Regulatory Developments

Regulation will be the key driver of progress. Staying informed about policy changes can help investors anticipate shifts in the market.

Conclusion

Morgan Stanley’s view that Bitcoin on US bank balance sheets is coming but not yet captures the current state of the financial landscape. The momentum behind Bitcoin adoption is undeniable, driven by institutional demand, technological advancements, and competitive pressures. However, significant hurdles remain, particularly in the areas of regulation, risk management, and accounting.

The transition will not happen overnight, but the groundwork is already being laid. As regulatory clarity improves and infrastructure continues to զարգ, the integration of Bitcoin into traditional banking systems appears increasingly inevitable. For now, patience is key—but the direction of travel is clear.

FAQs

Q. Why does Morgan Stanley believe Bitcoin will be on bank balance sheets?

Morgan Stanley sees strong institutional demand, improving infrastructure, and growing regulatory clarity as key drivers that will eventually enable banks to hold Bitcoin directly.

Q. What is preventing banks from holding Bitcoin right now?

Regulatory uncertainty, Bitcoin’s volatility, and accounting challenges are the primary barriers preventing immediate adoption.

Q. How are banks currently involved with Bitcoin?

Banks are offering services like crypto custody, trading, and advisory, allowing clients to gain exposure without holding Bitcoin on their balance sheets.

Q. Will Bitcoin become a standard asset for banks?

While not guaranteed, the trend suggests that Bitcoin could become a common asset class for banks as the market matures and regulations evolve.

Q. How can investors prepare for this shift?

Investors should focus on long-term strategies, monitor regulatory developments, and understand the evolving role of Bitcoin in the financial system.